Sale-leaseback 101

What it is, why it’s advantageous and when to execute

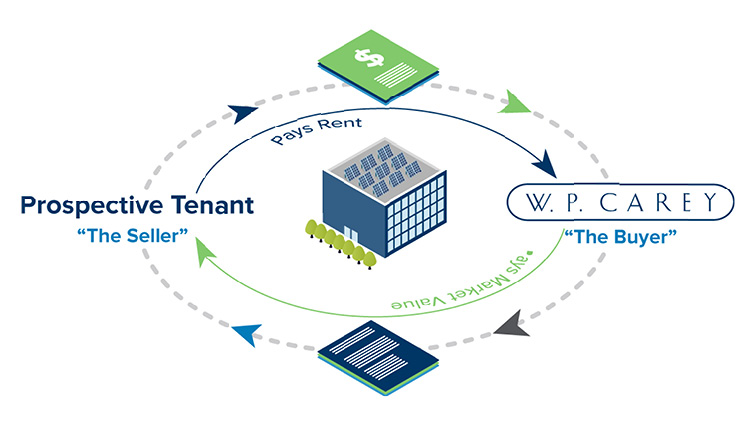

What is a sale-leaseback?

The concept is simple. For many companies, their real estate represents a significant cash value that could be redeployed to fund their core business operations and growth strategies. Through the “sale and leaseback” model (or sale-leaseback), a company sells its real estate to an investor for cash and simultaneously enters into a long-term lease with the new owner. In doing so, the seller extracts 100% of the property’s value and converts an otherwise illiquid asset into working capital, while maintaining full operational control of the facility.

What are the benefits?

There are many reasons why a company would consider monetizing its owned real estate. Sale-leasebacks offer companies an alternative to traditional bank financing. This is particularly advantageous during periods of uncertainty—as seen during COVID-19 when conventional financing was limited, especially for sub-investment grade companies.

Whether a company is looking to invest in R&D, expand into a new market, fund an M&A transaction or simply de-lever, sale-leasebacks serve as a strategic capital allocation tool to fund both internal and external growth in all market conditions.

Key benefits include:

- Immediate access to capital to reinvest in core business operations and growth initiatives with higher equity returns. We like to say that most businesses are not in the business of owning real estate. A sale-leaseback enables companies to focus on its core competencies, while capitalizing on the value arbitrage between the real estate valuation and the company’s EBITDA multiple.

- 100% market value realization of otherwise illiquid assets compared to the 65% to 75% of the appraised value that a typical mortgage would garner.

- Limited financial covenants, unlike some debt instruments, providing the seller with greater control over its operations.

- Alternative capital source when conventional financing is unavailable or limited.

- Retainment of operational control with no disruption to day-to-day operations.

- Potential tax benefits by deducting rental payments rather than being subject to interest limitations for traditional debt as defined by tax laws.

Why now?

Record level dry power, coupled with today’s low interest rate environment continue to drive investor demand for alternative investments such as real estate, pushing property values to all-time highs. These conditions make now an opportune time for sellers to maximize their proceeds and secure favorably priced, long-term capital via a sale-leaseback before interest rates rise again.

In conclusion

Key to the success of a sale-leaseback arrangement is finding an experienced and well-capitalized investor who can understand the unique requirements of each seller and structure the lease accordingly. When working with an investor like W. P. Carey, sellers have the added advantage of gaining a long-term partner who can support its tenants through long-term flexibility and additional capital should they wish to pursue follow-on projects such as expansions or energy retrofits as their business and real estate needs evolve.

Related Topics:

You May Also Like:

Why Build-to-Suits Are Gaining Momentum in Today’s Market

As companies navigate an increasingly complex operating environment, one theme is becoming clear across the industrial and logistics sectors: flexibility and tailored real estate matter more than ever. Against this backdrop, build-to-suit development is gaining renewed momentum—emerging as a strategic solution for occupiers seeking custom real estate that aligns with their business needs. A Market Defined by Constraints and Opportunity Today’s market conditions are creating a natural tailwind for build-to-suit projects. In many logistics hubs, available space is limited, while demand for high-quality, well-located facilities remains strong. At the same time, elevated construction costs and shifting supply chains have slowed speculative development, further limiting available real estate. For occupiers, existing real estate often falls short of increasingly complex operational requirements. Whether driven by automation, inventory optimization or last-mile delivery needs, companies are prioritizing facilities that are tailored to their business from day one. Build-to-suits bridge this gap—offering a direct path to purpose-built space in markets where alternatives are limited. The Shift to Purpose-Built Real Estate The increase in demand for build-to-suits reflects a broader evolution in how companies view real estate. Rather than adapting operations to fit an existing building, occupiers are increasingly designing space around their workflows, equipment and long-term growth plans. A build-to-suit is fundamentally a partnership model: a developer or capital provider funds and delivers a custom facility aligned with a company’s specifications, with the company entering into a long-term lease upon completion. This approach has several key advantages: Customization: Facilities are custom-built for the tenant’s needs and designed to optimize layout from the outset Capital efficiency: Companies can preserve capital for core operations rather than investing in real estate Operational control: Tenants maintain operational control of the real estate Scalability: Properties can be designed with future expansion, sustainability improvements or evolving requirements in mind In a market where efficiency and resilience are paramount, these benefits are becoming increasingly compelling. Aligning Real Estate with Supply Chain Strategy One of the most significant drivers behind the growth of build-to-suits is the transformation of global supply chains. Companies are rethinking their networks to improve resilience and proximity to end customers, placing greater importance on the role of real estate within their broader strategy. As a result, modern logistics facilities are no longer just warehouses; they are highly specialized hubs incorporating automation, advanced power requirements, specialized layouts, sustainable features, and strategic proximity to population centers and key transportation routes. As these requirements become more complex, custom build-to-suit development is increasingly the most effective—and sometimes only—option. Momentum That’s Here to Stay What began as a niche solution for highly specialized occupiers is becoming a mainstream approach across industries. From e-commerce and third-party logistics providers to manufacturers and retailers, a growing range of companies are turning to build-to-suits to meet their evolving real estate needs. At W. P. Carey, we see this trend as a reflection of how occupiers increasingly value partnership. Through our Carey Tenant Solutions platform, we work alongside tenants to design, fund and deliver tailored real estate solutions that align with their operational goals. By combining deep expertise with a partnership-driven approach, we help companies turn real estate into a strategic advantage—built for today’s needs and adaptable for the future.

Net Lease Retail Continues To Surge

Net lease retail continues to attract investors seeking stability, long-term income, and defensive retail plays, and market momentum should remain strong into next year, experts say. GlobeSt spoke with Michael Fitzgerald, Head of U.S. Retail Investments for W. P. Carey, at this year's ICSC Las Vegas conference to discuss which retail categories are strongest, why sale-leasebacks continue to dominate the landscape and why he remains bullish on net lease retail. In this video, you'll hear: Which retail categories are the strongest in the current market What's driving the growth of sale-leaseback transactions How the net lease market will perform in 2027 Watch now An interview with Michael Fitzgerald, W. P. Carey, and Holly Amaya, GlobeSt.com.

Net Lease Retail is at an Inflection Point

As retail investors and operators convene in Las Vegas for ICSC, the conversation around net lease retail feels both familiar and different. Familiar, because the net lease retail market continues to demonstrate resilience and stability. Different, because the drivers shaping today’s retail real estate decisions are evolving—creating new opportunities for operators and investors alike. From rising sale-leaseback activity tied to M&A, to more intentional approaches around store size and format, today’s net lease retail market is being shaped by a combination of strategic growth decisions, changing consumer behavior and a more balanced transactional environment. These are several of the key trends taking center stage ahead of the conference. Sale-leasebacks Follow Strategic M&A Activity One of the most consistent drivers of sale-leaseback volume in retail today is merger and acquisition activity. Whether it involves private equity-backed platforms consolidating regional brands or strategic buyers acquiring complementary concepts, transactions often prompt companies to reassess their balance sheets—and real estate frequently emerges as one of the most efficient sources of capital. In many cases, companies come out of acquisitions with real estate portfolios that were not central to the strategic rationale of the deal. Sale-leasebacks allow operators to unlock that capital, streamline their asset base and redeploy proceeds into higher-return priorities such as new stores, technology investments or debt reduction. What stands out in the current environment is that this activity is not limited to highly leveraged situations. Healthy, growing retailers are increasingly using sale-leasebacks proactively as part of longer-term capital planning, particularly when M&A introduces scale or accelerates geographic expansion. Sale-leasebacks continue to provide a compelling alternative to traditional financing for businesses seeking flexibility and predictability. The Evolution Toward Smaller, More Flexible Footprints Another defining trend across retail is the ongoing evolution of physical store footprints. While large-format locations remain relevant in certain categories, many retailers are gravitating toward smaller, more efficient concepts that align with omnichannel strategies and localized demand. These stores are often designed to serve multiple functions—acting as showrooms, service hubs, fulfillment points or a combination of the three. Flexibility has become increasingly important, both in store design and in location strategy, as retailers respond to shifting consumer behavior. From a net lease perspective, this evolution places greater emphasis on unit-level fundamentals. Smaller footprints can generate compelling cash-on-cash returns, but success depends heavily on the alignment between location, concept and the operating model. The underwriting process for net lease retail investors is therefore increasingly focused on how these formats perform across markets, how scalable they are and how they fit into a retailer’s broader growth strategy. Stabilized Cap Rates Bring Predictability Back to the Market After a period of volatility driven by rapid interest-rate movements, cap rates across the net lease retail space have begun to stabilize. While pricing discipline remains essential, the return of predictability has had a meaningful impact on transaction activity. Clearer valuation benchmarks make it easier for buyers and sellers to transact. Investors can underwrite opportunities with greater confidence, tenants can assess capital alternatives more thoughtfully and deals are less likely to stall amid uncertainty around pricing expectations. That said, credit quality, location fundamentals, lease structure and real estate criticality remain core considerations. However, in a more balanced environment, high-quality assets supported by strong operators are finding liquidity, and capital is moving more efficiently. Looking Ahead As ICSC Las Vegas approaches, there is optimism across the net lease retail landscape. While uncertainty remains part of the broader economic backdrop, the conversations in Las Vegas are expected to reflect an industry that has evolved through recent cycles and continues to find opportunity through change. For net lease retail, the current environment represents less of a reset and more of a recalibration—one that rewards sound fundamentals, flexibility and a long-term investment approach.